Can the Free Market Rein in U.S. Health Care Costs? Step 2: Your “Health Insurance” Isn’t Insurance

It's time to stop pretending what passes for health insurance in the U.S. is really an insurance policy.

I apologize to all those who figured this out a long time ago. As a physician who went through four years of medical school and three years of residency, and had to suffer through a fair share of “The Business of Medicine” type talks and countless conversations with patients about their issues with health insurance, I somehow came through my training and many years of practice before I understood this most basic of concepts: what we call “health insurance” in this country is rarely insurance, and the unwieldy result creates all kinds of perverse incentives for expensive and low-quality health care.

I am grateful for the patient who finally broke it down for me a few years back. Insurance is all about covering uncertain losses — whether it be car, home, or term life insurance, the central concept is to prepare for a potentially catastrophic financial loss by paying manageable amounts of money in advance into a pooled risk fund. For those without profoundly deep pockets, taking out insurance policies often makes sense.

What gets termed “catastrophic” health insurance fits into this category; a healthy person can pay a low monthly premium and have coverage for a major, unexpected health event, like a heart attack, or, in my case, an unexpected cancer diagnosis. However, especially after the Affordable Care Act attempted to require comprehensive health care for all Americans, and outlawed traditional health insurance companies from holding pre-existing medical conditions against applicants (only age and smoking status can be factored into pricing), the vast majority of insured people in the U.S. do not have “health insurance;” instead, they have membership in what the Germans more accurately term their “sickness fund.”

Some prefer the term, “pre-paid health care,” which is the term my adopted state of Hawaii chose in their 1974 law requiring employers to provide comprehensive health plans to all full-time employees. Interestingly, this is how the bill is worded:

§393-2 Findings and purpose. The cost of medical care in case of sudden need may consume all or an excessive part of a person's resources. Prepaid health care plans offer a certain measure of protection against such emergencies.

“Sudden need?” “Emergencies?” It sure sounds like sensible old catastrophic care, but it’s not. Essentially, this was the forerunner to the ACA, requiring expensive comprehensive plans to cover all medical costs, both routine and unexpected. This is a “sickness fund,” replete with deductibles, donut holes, preferred networks, and so on. Healthy people pay in the same as unhealthy people, and thereby subsidize those with high annual expenses. It’s a uniquely American way of subsidizing a good; rather than relying on traditional concepts like those of greater means supporting those with less, the healthy, whether rich or poor, pay for the unhealthy, whether rich or poor.

Does this make sense? Of course not! More germane, the system created is riddled with perverse incentives and inefficiencies. However, we let ourselves descend to this place over many decades of strange policy.

Unsurprisingly, our current dilemma stems from a mix of government interventions and “free market” responses. In 1942, President Roosevelt instituted a wage freeze due to inflation concerns in the wartime labor market; this incentivized businesses to compete outside of wages, often by offering health insurance plans, at the time lightly utilized. A year later, the IRS opted to exempt such business expenses from taxation, creating a major incentive for businesses to offer such plans instead of, say, higher wages, as a means to compete for employers. In 1954, with the deduction under threat from the IRS, under President Eisenhower, Congress passed legislation that contributions to health insurance would remain tax-free.

From 1940 to 1950, the proportion of Americans with some form of health insurance went from under 10% to over 50%, and has grown since. The advent of Medicare and Medicaid in the 1960s, and now the ACA, has led to over 90% health plan coverage in the U.S. The ACA essentially transformed “catastrophic” plans into comprehensive plans with high deductibles, and largely limited them to people under 30; if the covered biologic medication for your autoimmune disease runs $35,000 per year, you can still sign up for a relatively inexpensive “catastrophic” plan, pay your maximum $10,000 or so out of pocket, and have the plan pick up the other $25,000 in utterly expected costs — not exactly the core premise of insurance.

With health care plans essentially all of the comprehensive variety now, we have a situation fairly unique in the world, in which half of our citizens receive “prepaid health care” from an employer, and we walk about like this makes perfect sense. It does not!

For one, rational employers now have to consider factors that have no innate place in the labor market. Our most recent insurance quote to cover employees would charge $600/month for a 55-year-old worker, but only $300/month for a 30-year-old employee. Our system is forcing me either to be ageist or irrational. It also pushes business owners to hire part time employees whether or not that best meets their needs; that 55 year old employee immediately starts costing an employer an extra $6-7/hour the moment they cross from 19 hours/week to 20 hours/week (in Hawaii; nationally the threshold under the ACA would be 30 hours). These are substantial amounts, especially for entry-level positions. I don’t think it’s controversial to posit that financially penalizing full time positions is bad economic policy.

Then there’s the more basic issue: why should businesses be the ones left to insure individuals’ medical needs? It creates an additional layer of opacity and negotiation, further removing the average health care consumer from the the actual delivery and cost of their care. It feels very American and “free market” to say things like, “We’re one of the only modern economies to rely on businesses to provide health care for their employees;” but really it’s a confession, a confession that we aimlessly drifted into a nonsensical system running against the market forces which might actually lead to a more efficient health care system.

Part of efficiency stems from transparent pricing; I covered that in Part 1 of this series. Another huge step would come from no longer pretending that our “sickness funds” are actually insurance, and let the market work out the costs of real health insurance, the kind that covers unforeseen substantial medical costs. Spoiler alert: such policies will not be expensive.

Under the aforementioned ACA rules, catastrophic care plans are limited to young people who think they can afford a relatively high medical hit given their high deductibles. In other words, while not being able to discriminate against pre-existing conditions, this is otherwise the lowest risk pool allowable by law. Costs are fairly low; here are the plan options from our local BCBS, with the catastrophic plan highlighted:

What a deal! As long as you are ready to handle $9100 per year in covered expenses (God forbid you get into a lot of non-covered expenses; that’s another place where price transparency comes into play), you get clearly a better plan than the Bronze options, for less than half the price. This is due to the patient pool being made artificially low risk in this cohort because of the mandated low average age.

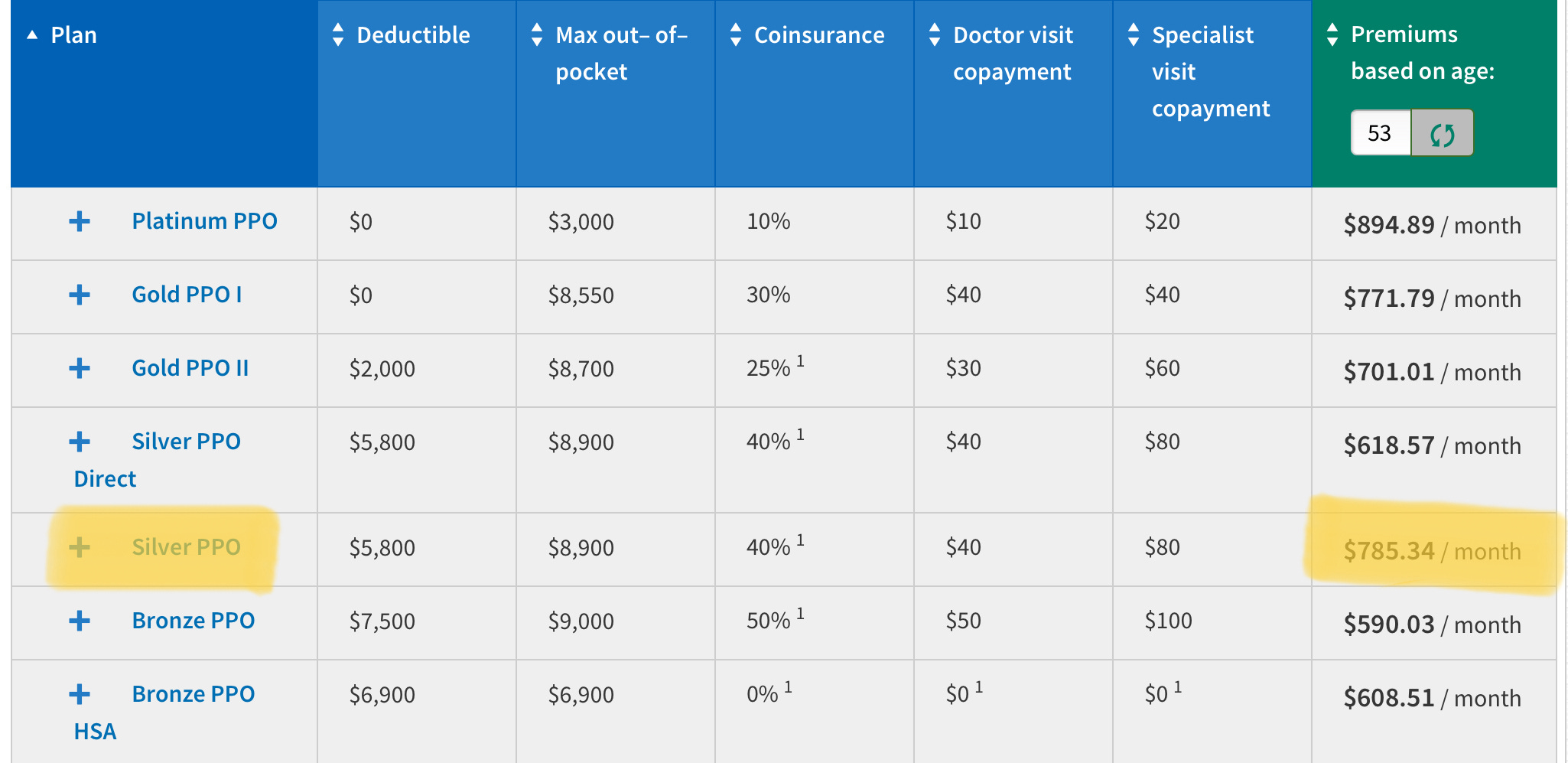

Increase to the ripe old age of 53, eliminate the option to join the low risk pool of the catastrophic plans, and despite my perfect health when I was shopping back in July, prices are… higher; a lot higher:

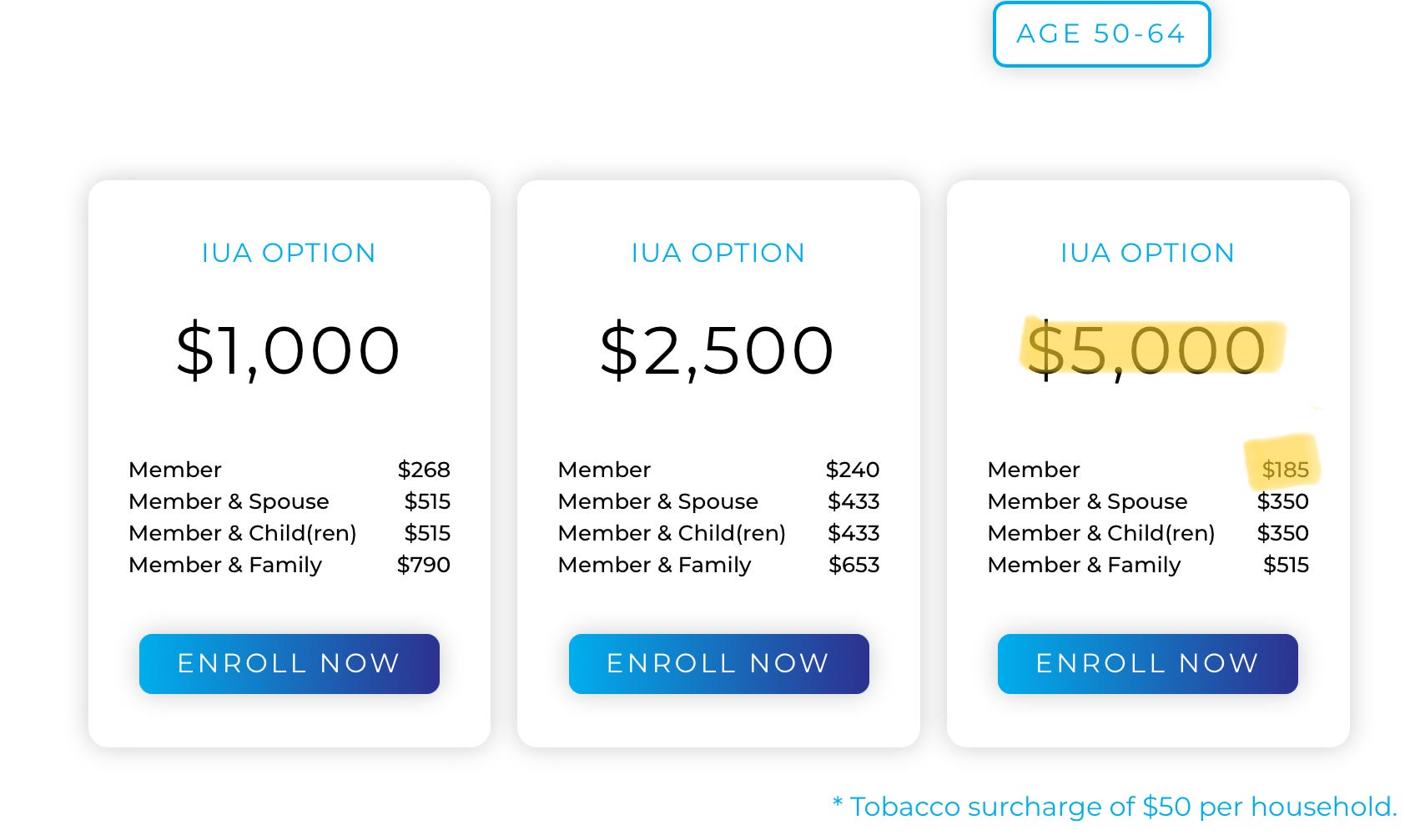

The silver plan is a pretty crappy option; for almost $800/month you get a $5800 deductible (which is more than the 60% of U.S. families who could not handle an unexpected $1000 bill could manage), and a maximum out-of-pocket approaching $9000, plus terrible cost shares and copays. I highlighted it because the deductible and max out-of-pocket are the closest to the plan I actually ended up choosing: a “health sharing” plan from one of the faith-based companies who were allowed to enter this market within the ACA by expressly NOT declaring themselves to be health insurance. Of course, because up is down and 1+1=1, these plans are the only things actually resembling real health insurance! Now, I would be remiss if I failed to mention that these health sharing plans do not actually promise to insure your medical expenses, and apparently, sometimes they really don’t, which is a major problem! I did my due diligence with the company I chose, Zion Healthshare, and was convinced by their bottom line and friendly representatives that they would actually pay out in case of an emergency. Perhaps I was just lucky, but when I was diagnosed with cancer a mere three months after starting to pay into their system, they quickly validated my claims, and have paid every penny of my expenses after the $5000 deductible. (Note: I have no financial or other relationship with Zion Health, simply gratitude for their saving our financial bacon when my $200,000 oral cancer popped up out of the blue). This is how insurance is supposed to work! Here is what they charge us ancients between 50 and 64:

$185/month for that $5000 deductible, with the fine print adding that if three unrelated health events pop up within the year, the maximum out-of-pocket could reach $15,000. However, after the $5000 per event is met, there are no copays or coinsurance charges, and there is also freedom of choice to see any provider in whatever network one wishes. I make a decision, obtain a cash price and either pay it or alert my representative, and they reimburse me or pay directly. Refreshing; and roughly one quarter the cost of Blue Cross Blue Shield.

Of course, there are caveats. Zion paid out around $50 million in 2022; add another zero and I’d feel better about their stability, and given that health sharing plans are not held to the same standards as insurers, the doomsday scenario of having a huge, legitimate medical expense and not being reimbursed is more real than with a BCBS plan. If large players were allowed to enter this market, however, this concern would be minimized. More importantly, the reason Zion can charge so little and still function as a business is because they only accept low risk health consumers; if you have a pre-existing condition, you have to wait a specified period before you can appeal for reimbursement. Otherwise, it would be like applying for flood insurance and expecting 100 year flood zone rates after building in a 5 year flood plain.

True health insurance of this nature, in which both routine and unexpected costs related to pre-existing conditions are not covered, will not serve the third to half of Americans with known major health problems. It will, however, provide truly affordable medical insurance for generally healthy people; and incentivize them via deductibles to shop for competitive prices for elective procedures, medications, imaging, and the like, which provides downward price pressure for everyone’s benefit.

All of us should be required, or at least deeply incentivized, to have a catastrophic health plan. Hospital chains could require insurance to treat elective issues; or states could induce their citizens to do so. For goodness sake, if we are required to sign up for car insurance just to drive a car off the dealer’s lot, surely we can figure this out, too. The advantage is that the ability to afford medical treatment at the time major problems arise has positive externalities for society at large: a healthier and more productive population. (I will steer clear of so-called preventative care for the moment, since my personal opinion is that it accomplishes remarkably little and generally does not save money.) What’s more, with hospitals no longer having to write off substantial portions of their operating expenses due to uninsured patients unable to pay their big ticket medical bills, they could choose to bring their prices down for the rest.

In any case, there remain three large elephants in the room: what about people who qualify for, but cannot afford, even an inexpensive catastrophic plan, or a moderate deductible? More importantly, what do we do with all the people with chronic disease? Finally, if we are to shift the burden of paying for so much of our health care away from employers to individuals or government, how do we accomplish this transition in something resembling a fair and reasonable manner?

Such concerns, dear reader, will be the subject of Part 3. Libertarians, any warm feelings I may have evoked with the first two parts of this series are going to take a hit. At its core, I don’t think this country is ready to return to Charles Dickens’ England, where Tiny Tim needed to await the largesse of Ebeneezer Scrooge to afford medical treatment. Americans think everyone should have access to health care.

Someone is going to have to pay.

This is really helpful to read and insightful. It should be mandatory reading. In fact, It's time for a podcast. Maybe you should actually get into politics. Yes, it is possible to make a difference, with slightly higher probabilities than the Steelers winning a super bowl.

Buzz I really enjoyed #1 and #2 of your cogent analysis.

I think you are benefiting, in part, from having worked for government care, current care, and now a version of concierge care. Look forward to #3.

I am still in Private Practice (non owned) Cardiology, so if I had price clarity I could do something.

Also thanks for explaining that in particular Medicaid is not insurance and does not cover expenses so it remains in part a Charity at least for those outside government pay systems.

JAM