Can the Free Market Rein in U.S. Health Care Costs? Step 1 - Price Transparency

First of a three part series pondering how to get ourselves out of the mess we're in, without abandoning free market principles.

The U.S. health care system is an utter and complete mess. I say this as a physician who has functioned both in its center and on its fringes over the past 20 years, and has been mulling how best to reform it for almost as long. Most people understand that the system needs to be revamped. The question in dire need of an answer is: how best to do it?

I won’t waste much space making the case for the excesses of our system when it comes to cost. One graph does it well enough, here from our friends at Peterson-KFF:

Half! That’s remarkable. The average U.S. family spends almost $22,500 a year just on health insurance premiums, and medical expenses are the cause of about two-thirds of all bankruptcies in the U.S.

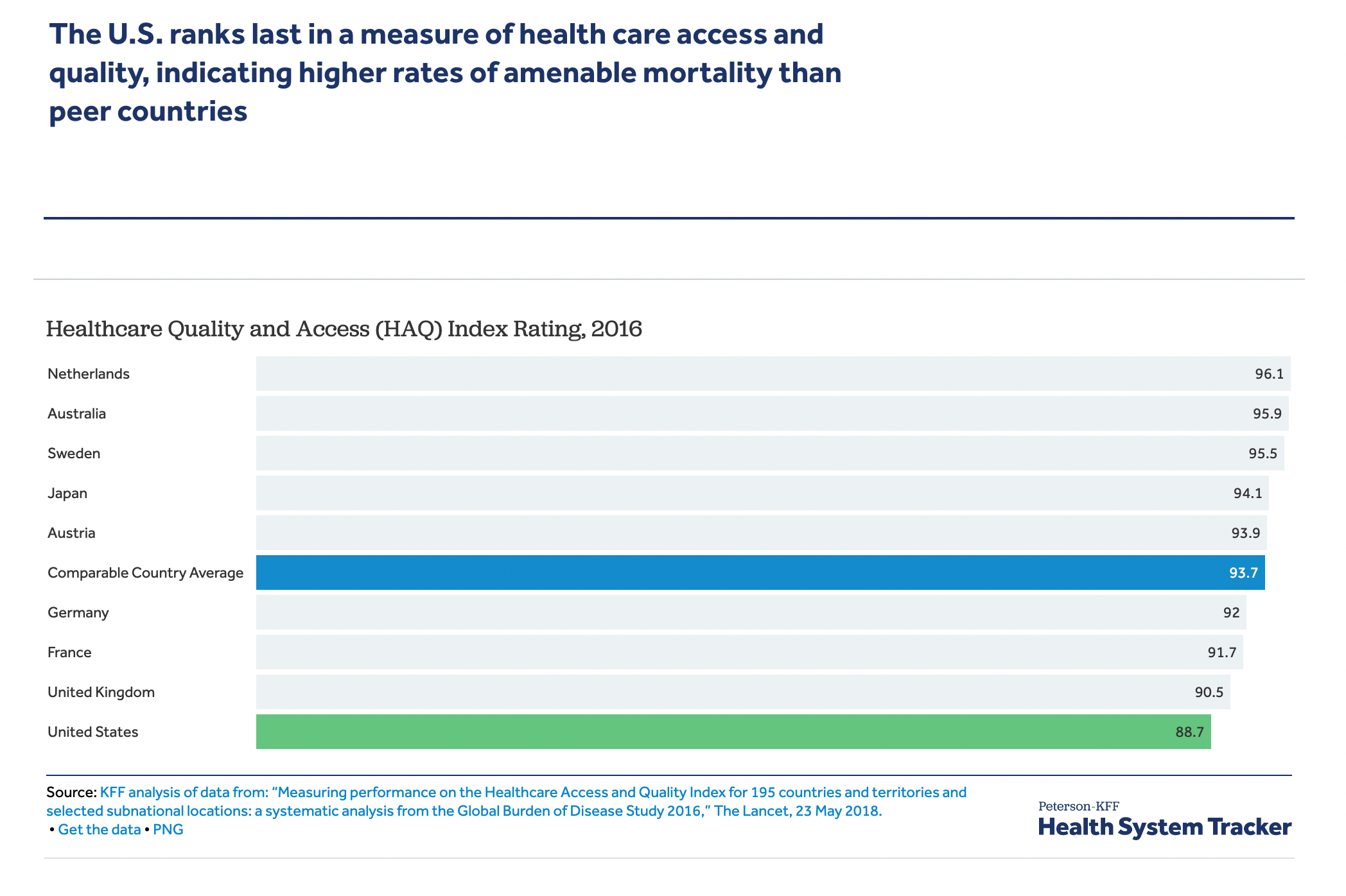

Of course, for all that money, we end up with unremarkable outcomes in terms of benchmarks like longevity, infant and maternal mortality, and health care access. In one chart, again from Peterson-KFF:

I don’t pretend this implies that we are wasting all of the money we spend on health care in this country. There may be certain structural aspects to U.S. society that predispose us towards poor outcomes. We also do some things quite well here, especially in the realm of cutting edge surgeries and adoption of new medical technologies. However, it’s hard to pretend that we need to be spending all this money, nearly 20% of our GDP in 2020 (up from 9% in 1980!), given the apparently modest return on investment.

Most importantly, the current formula is unsustainable. While the players with a vested interest in maintaining the status quo are well known and thought to be nearly untouchable given their sheer size (the hospital and health insurance industries, American Medical Association, and Big Pharma, chief among them), the reality is that the economics are sufficiently dismal that we are unlikely to have much choice beyond substantial change in the intermediate-term future. The frequent discussion of Single Payer/Medicare for All throughout the last Democratic Party primary speaks volumes to the perceived need for change.

As someone reluctant to put this all in the hands of the government, though, I am hopeful that reasonable alternatives exist. Having grappled as a physician with the monolithic entity known as Medicare for too many years, I find it rather terrifying to confront a future in which Medicare is our health care system. However, the current system is bad enough that I honestly think a “Medicare for All” type approach might be an improvement. For goodness sake, though, let’s try to think through a better solution.

The first step I propose is real price transparency. No, not the mediocre and largely ignored attempt framed in the Hospital Price Transparency rule that ostensibly was to kick in by 2021. Its scope is too small, it lacks a real enforcement bite, and it allows far too much leeway to hospitals in terms of how to present their data. This particular legislation has largely proved useless.

What would be helpful is a system in which all health care providers are required to post their prices for every given service in a clear, apples-for-apples manner. You know, kinda like… almost everyone else who provides a service. We are so very far away from this ideal in our current reality.

When I left the community health center on rural Hawaii Island where I had worked for the first seven years after residency, I joined my wife’s cash-pay practice 20 minutes up the road and opted to keep working with insurance of all types. One of my first orders of business was to agree on my rates offered and sign contracts with each of the dozen or so insurance providers in this small state. The next was to hire a firm to handle our billing of these insurances, since given its complexity, we otherwise would have had to hire another office worker. This cost us 8.25% off the top of all our reimbursements. Our billing company suggested we set the prices we formally bill Medicare at three times what they actually reimburse, since the occasional mainland insurance might actually reimburse at these rates! (We lacked the stomach to follow this advice, not wanting to appear like the archetypal greedy doctors when patients received their Explanation of Benefits after seeing us.)

Contrast that to our current system: in 2016, we switched to a “direct primary care” model in which we charge patients a fixed monthly fee outside of the insurance system. Everyone knows what they will pay over the course of a year for us to be their primary care doctors; however many visits, EKGs, or albuterol treatments they might require. That’s the simplest end of the transparent pricing spectrum, and not one our entire medical system should or could seamlessly enter. However, back when we were in the traditional fee-for-service, insurance-based model, we could easily have posted all of our prices. After all, we had fee schedules for every single thing for which we could possibly charge a patient, from a 30 minute visit to the nursing charge for an injection. More importantly, we, like most any private practice physician or hospital bureaucrat, understood which prices fairly compensated us. At Medicare and the local Blue Cross Blue Shield reimbursement for a 30 minute visit, about $110 back then, we could get by if we kept the schedules full, able to pay overhead and keep the doors open, if not quite earn a normal physician’s salary. Medicaid’s $70? Absolutely not. Give me a free weekend back then, and I could have posted rates for all of our services that would have been fair and reasonable; a little higher than others since I prefer to spend more time with patients than most doctors, but the market could have sorted out whether I was worth it.

And that, really, is the first step towards controlling costs in this health care system, short of simply having the government set all the prices: make them clear. The analogy often used to lampoon our current system is the distinction between car insurance and health insurance. Can you imagine if car insurance was required, not just for catastrophic events, but for buying gasoline? Of course, gas stations would not post the prices of gas; that would be independently negotiated with every car insurance company, and the consumer would not know exactly how much their company was being charged by the different stations. At the end, you might deposit your copay, and, a few months later, receive a notice of how much you paid, how much your insurance paid, and, sometimes, how much you still owe for uncovered expenses (perhaps the station you chose was “out of network,” or your 20% copayment could only be calculated with the final billing).

The whole notion sounds utterly absurd, but that is essentially how we do business in U.S. health care. This New York Times article cited multiple examples where the range of charges for the same service from one insurance company to another to the cash-pay price could be three or four fold different; I can confirm that similar cost spreads exist in the area where I practice. A 2016 survey published in the American Journal of Cardiology found that among over 50 hospitals, the cost given for a heart bypass ranged from $45,000 to $450,000, with no association with quality of care!

To make matters worse, extending the car insurance analogy to the pharmaceutical industry, the gasoline prices, too, would be independently negotiated with large swings between stations and outsized retained profits by “benefit managers”. To describe the system as “inefficient” is kind.

Now, I am not so naive as to believe that price transparency will single-handedly save our health system from spiraling costs, and many have pointed out its limitations. This is a three part series, after all. However, setting a single price for a single service is a necessary first step, and one that can be done with a minimum of expense and pain. The price would be the price; cash-pay patients would face the same charge as insurance companies. Insurers could balk at including in their plans care providers with outlier prices, and could threaten to cut out participation for elective services with hospital systems charging unusually high rates for emergent care (an admittedly thornier issue). Pharmaceutical firms will have to name their single price for their medications; no more back-office negotiations between middlemen and insurers that leave multiple, inscrutable prices for every drug. Everyone in the health care landscape would know what everything costs.

If we are to create a true health insurance system in this country (the subject of Part 2), clear and reasonable prices are an essential starting point. And, while many dismiss the value of price transparency as not inherently addressing the primary problem in our country — our health care prices are simply too high! — I am old-fashioned and believe that knowledge is the first step to wisdom.

Once every provider of health care is required to post their charges in a consistent manner, journalists, trade groups, consumer websites, and the like, can tee off on those with outlier prices. True, not every health care consumer has the savvy or access to utilize this information. However, we doctors are the ones who order almost all the consumables in the health care economy. What if the Electronic Health Records we all use now are required to post price alternatives for every lab or procedure we order? My basic EHR already includes a rudimentary version of this software whenever I order a medication for a patient, giving cash pay and co-pay amounts (of course, it sometimes fails because of the layers of complexity in some of these pricing plans, which price transparency would eliminate). Yes, integrating price information from area labs and imaging centers into an EHR will take a little time, but nothing a proper 17 year-old programmer could not handle from their parents’ basement.

I know from personal experience that seeing the cost of what we order as physicians affects what I order. I rather prefer knowing both a ferritin and an iron panel when concerned for a patient’s iron status, for instance, or a free and total testosterone level if working up a patient with fatigue and decreased libido; but when I learned that ordering both tests essentially adds $100 to either work-up, I have tried to make sure I really need the extra information before ordering both. I won’t pretend I have hard evidence that my colleagues would act similarly; while a Johns Hopkins study saw a modest decrease in lab orders when their hospital physicians were exposed to actual lab prices, the practice did not change hospitalist behavior at Penn Medical when ordering inexpensive inpatient tests for their patients. However, if I am sitting across my desk from a patient who needs a knee MRI and we see that the local hospital would charge $2000 for the study with a $400 copay for the patient, while the nearby free-standing imaging center would only charge $1000 with a $200 copay — I think that knowledge would change behavior.

We actually have a study reviewing a similar scenario, and the results were somewhat concerning for believers in the primacy of pricing. Ivy League researchers studied the determinants of choice of venue for lower leg MRIs and proximity to patient or price, even in a high-copayment cohort, were not the primary drivers; overwhelmingly it was the doctor’s recommendation. Of course, in this real-world study, doctors were not given the prices at the facilities to which they referred patients; I want to believe this would make a huge difference in referral patterns. Cynics might point out that we have tales of hospital systems leaning on their physician providers to prevent “leakage” of expensive services out to other facilities, and many physicians would continue to refer in-house to avoid threatening emails from their middle managers even if they knew their patients would suffer higher costs. To this I say: any doctor so spineless as to kowtow thusly to bean counters needs to find another profession; and, more importantly, the goal of price transparency is to pressure high-priced systems (often hospital-based) to lower their prices, thereby making this sort of abuse less costly.

An easy trap to fall into when pitching the value of price transparency in medicine is related to the above example; we tend to talk about things like choosing MRI facilities and hip surgeons, the so-called “shoppable” services, which lend obvious appeal to price transparency — examples in which consumers have agency around their choices. Unfortunately, it’s possible that only about 40% of health care expenses truly fit in that realm. It’s still possible to build models showing substantial savings (up to $80 billion!) just by encouraging lower prices within this subset of health care expenditures; but medicine has taught me to take models with a grain of salt. We don’t have much ability to shop around for the cheapest area ER or vascular surgeon when our doctor tells us our foot has gangrene.

However, hospitals will have to post their inpatient charges, too. If you want to list a $500 charge for administering a tylenol, be prepared for some feedback. More innocuously, if a knee MRI runs triple that of a nearby imaging center, expect that area stakeholders — consumers, insurance companies, employers, and the government — will want to hear why your MRIs are three times more valuable than the competition’s. It’s harder in the case of the roughly 20% of hospitals, mostly rural, who lack competition, but they can still be held to regional standards. As a parent and physician, I try to steer clear of shame as a method to foster change; but in the world of medical economics, I see the value.

I will finish by saying that the current system, aside from being inefficient and confusing, simply is morally wrong. It is wrong that a patient can go in for a common outpatient procedure like a hip replacement and not know how much they, or their insurance, ultimately will be billed, especially since the amounts can be life-altering in a country in which 60% of its population is unprepared for an unexpected $1000 expense. It’s wrong — and more than a little crazy — that when I was asked to pre-pay for my radiation treatment two months ago by a major hospital I was quoted a price of $22,000 “for the entire treatment”; and was then later billed another $28,000; and now another $80,000!

This madness has been tolerated for too long. It’s unethical and inefficient. Change will be hard; those who profit by this bloated multi-trillion dollar system have too much at stake. However, as we approach the fork in the road at which we can no longer afford our health care system, we’ll be left with two choices: let the government fix the problem, or see if the free market can be enlisted to do so. My bias is that that the government should only be chosen as the very last resort to solve any problem.

I consider this post an opening salvo rather than any firm ideology; I look forward to reader comments to continue this discussion. Part 2 will address how most of us missed the memo that “health insurance” is hardly insurance in the U.S. at this point, and the cost we pay for tolerating our bizarre hybrid system of health care payment.

Back in the mid-60s I had my first experience needing to see a GP in the small Maine town were I lived.

I'll call the now long gone physician "Dr. Smith" but only because at my advanced age there are black holes in my memory bank.

Short story long, Buzz, I asked my neighbor on the other side of the valley how much Dr. Smith charged.

She literally gave me a few dozen fresh eggs and a large bag of produce in case I was low on cash.

Everyone in Winterport, Maine knew I was just starting out as a writer of obituaries for the local newspaper.

I had a painful sinus infection that laughed at aspirin.

Dr. Smith turned out to be a fellow in his mid-50s, and told me my neighbor had called him to explain my lack of ready cash. I went out to my ancient jalopy and returned with the eggs and produce.

He chuckled, and I winced.

A dose of warm salt water in each nostril followed by a lot of nose blowing brought me some relief.

Doc Smith thanked me for the eggs and produce, and advised me to start learning how to become a newspaper reporter so I could one year soon give him cash.

He became my family doctor from that day forward until his passing several decades later.

His passing was mourned by the entire town.

My last position at the newspaper was as the business and technology editor, where I soon understood most of the people I interviewed made far more money than I found in my weekly pay envelope.

I left the newspaper in 1979 to start several companies that created software for the then new type of computer we called micro computers, and are now called cell phones.

As a long retired entrepreneur, I wish you well in trying to solve the problem of what I can only describe as a disaster for our citizens who are at the lowest levels of wealth.

Seems as though your recovery is going well, if only because you are now returning to writing essays that expose your inner gad fly 😏

Look forward to parts 2 and 3.

Having no prices, allows for cost shifting.

Most consider insurance to be coverage for 'health' instead of 'a way to pay'.

Thus either pay 4-5x (I've seen bills 200x) based on the infamous 'charge master'

The 'charge master' is a 'private' doc that prices services at 4-5x+ for 'cash'

Logically, if one was paying up front, there would be less paperwork and cost should be less.

Solution: Anti-trust <understand there are exemptions in law as of now>....Just as Microsoft was not allowed to charge IBM more then Dell for the same Software, Hospitals and providers should not be allowed to charge patients more then insurers for the same services.

It is true that Microsoft is able to offer volume discounts....thus a company committing to a larger purchase will get a slightly better price verses purchasing one. These have to be posted and available to all (meaning a group of individuals forming a purchasing entity: committing to the same price level as an insurer.) The price difference is maybe 25% less for the largest companies sliding down to list price for small business or one person. VERY different then 400 to 500% plus if you don't pay the mandatory health insurance kickback.

Having the same (small volume difference allowed) prices would solve so much of the bankruptcy problem. MORE people can pay (with small loans, charity, etc) a $10k charge....they can't pay a $50k to $100k charge.

Easy to implement: ALL prices public. Legal to discuss. People can compare. If charged differently then hospital / Dr. etc. fined. Person doesn't get for 'free' <avoid lawsuit BS: not about enriching individuals>, the individual does benefit by getting (and pay) the public price. The fine is paid by the hospital and used for general public benefit (e.g. free public services | pay for the service below). The mistake charges are made public (individual privacy) and the CEO of the hospitals or CFO is held responsible and also fined.

Since prices are 'public', the cost doesn't have to be hiring a lawyer. There can be a central neutral group created to review (at no cost to individual or a small cost (refunded if the person was charged incorrectly. This process Incentivizes people to only submit if incorrect))

The 'charge master' allows hospitals etc. to claim tons of 'charity care' and deductions all based on rates that insured are not charged.

This is by design by Big Pharma and the Medical establishment. Have the government pay for as many as possible (insurance), have the person never question the costs (insurance pays), never consider alternatives (sorry: I have 'insurance' and alternatives are not covered...I'd have to pay out of pocket!) Rockerfeller medicine at its finest (sarcasm)